On March 27, 2025 the IRS’s Advance Pricing Mutual Agreement Program (“APMA” or the “Program”) released Announcement 2025-13 which provides APMA’s annual Advance Pricing Agreement (“APA”) report (the “Report”). Key takeaways and our observations are noted here.

APA Completions Slightly Down; Completion Times Improved

Overall, the Report indicates strong performance and generally efficient resolution of APAs by APMA in 2024. The total number of APAs concluded – 142 – was lower than the record of 156 concluded in 2023, but still among the highest recorded in APMA history and the second highest number of APAs concluded in any year over the 10-year period of 2015-2024. It should also be noted that APMA concluded only 77 APAs in 2022, which in turn suggests that the record of 156 APAs concluded in 2023 may have been attributable in part to the clearing of a backlog. Three-year APA completion totals for 2022-2024 are summarized in the table below.

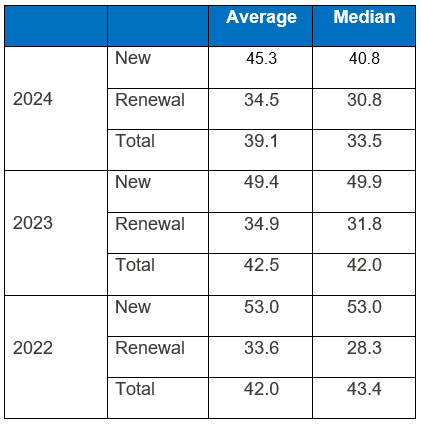

During 2024, APMA also decreased its average completion times for APAs to 39.1 months (down from 42.5 in 2023) and median completion times to 33.5 months (from 42.0 months in 2023). The decreased completion times appear attributable to a combination of (i) a higher percentage of completions that were renewal APAs in 2024 (58.5%) as compared with 2023 (47.4%), and (ii) significant decreases in APA completion times for new APAs to a median of 40.8 months in 2024, a decrease of over 9 months from the 2023 median completion time of 49.9 months.

Three-year average and median case completion totals for 2022-2024 (in months) are set forth in the table below:

APA completions and completion times are not dispositive measures of APMA performance since these statistics alone do not take into account the difficulty and level of sophistication of the APAs concluded in a given year. In this regard, the Report provides mixed indications of the difficulty of cases concluded in 2024 versus 2023. On the one hand, in 2024 APMA concluded considerably more Multilateral APAs – a record of 10 in 2024 versus 2 in 2023, and fewer Unilateral APAs – 13 in 2024 compared with 24 in 2023. This is noteworthy because all else equal, Multilateral APAs can be the most-resource intensive APAs in APMA’s inventory (due to the need to engage more than one treaty partner) while Unilateral APAs are the least-resource intensive (since no treaty partners are involved). As a further indicator of the sophistication of APAs concluded in 2024, the Report indicated that 22% of completed APAs involved the use of intangible property, an increase from 18% of completed APAs in 2023. As the Report notes, such APAs involving the use of intangible property “can be among the most challenging transactions in APMA’s inventory.” But on the other hand, the Report also indicated that 2024 completions contained a higher percentage of renewals (58.5%) than in 2023 (47.4%). All else equal, renewal APAs are generally less challenging and resource-intensive than new APAs because the prior APA generally provides a starting point for analysis.

It is also worth noting that in 2024, median APA completion times were significantly lower than average completion times for both new and renewal APAs. The higher average times are likely skewed by outliers that take a disproportionate amount of time as compared with a typical APA (which can happen for any number of reasons). The lower median times, on the other hand, provide confirmation it is often feasible to conclude an APA relatively efficiently, in many cases in less than three years.

Other Highlights

Some of the Report’s other highlights for 2024 include:

- As of December 31, 2024, total APMA staff was 126, up from 114 reported as of December 31, 2023. The reported headcount total as of December 31, 2024 was of course prior to the staff reductions (and possible further reductions) in 2025.

- APMA had continued success in closing cases with a number of treaty partners, including the top-three jurisdictions (for APA completions) of India, Japan, and Italy. In 2024, APAs with India comprised 29%, APAs with Japan comprised 23%, and APAs with Italy comprised 11% of bilateral APAs completed by APMA. Interestingly, this is the first time India surpassed Japan for the most bilateral APAs with the US.

- In 2024, 17 APA applications were withdrawn, which is a 30% increase from the 13 applications withdrawn in 2023 and an 83% increase from the 6 applications withdrawn in 2022 and in 2021. APA applications can be withdrawn for any number of reasons, and the Report provides no further insight for the reasons behind the increase.

- APMA’s Annual Reports demonstrate that year-after-year, APMA frequently concludes APAs with extended terms (longer than the “standard” 5-year term), and 2024 was no exception. During 2024, the 142 APAs concluded by APMA had terms ranging from 1 to 15 years, with an average term length of 6-years. This reflects APMA’s general practice to agree to additional APA years to the extent necessary to ensure that APA terms are sufficiently prospective in nature.

Challenges Loom but APA Demand Likely to Remain Strong

Looking ahead, 2025 will likely continue to be a challenging year for APMA with staff and other resource reductions, which in turn could result in increased case processing times. This may prompt some taxpayers to reconsider or defer APA requests. We remain hopeful, however, that staffing and other resource reductions could still be minimized if APMA is recognized as a vital customer service function of the IRS that helps to protect the US tax base through principled resolutions.

Nevertheless, APMA could also see increased efficiencies in the near future that may mitigate the impact of reduced resources. In December 2024, the IRS issued Notice 2025-04 in which it announced its intent to issue proposed regulations implementing the OECD’s simplified and streamlined approach (i.e., “Amount B”) for in-scope marketing and distribution entities. This approach, which functions as a safe harbor, could both make distribution APAs for in-scope entities more efficient and reduce demand for such APAs in countries that have adopted the approach. Another option to help alleviate demand for APAs is the International Compliance Assurance Programme (“ICAP”). This is possible if more taxpayers begin to view ICAP as a viable alternative to APAs for simpler, lower-risk transactions.

But on balance, we expect demand for APAs to remain high, driven largely by increasingly aggressive transfer pricing audits by numerous tax administrations throughout the world. We also expect APA demand to be kept high by new uncertainties that APAs can help mitigate (whether directly or indirectly), for example, the transfer pricing implications of proliferating tariffs in the United States and globally, and the interaction of transfer pricing and the Pillar Two rules that many trading partners are beginning to implement.

In any event, APAs will likely still prove in many cases to be the most efficient and effective path to certainty for many taxpayers that are willing to adopt a long-game strategy. This is especially the case when the many unique benefits of APAs are taken into account, such as the ability to efficiently resolve at least 5 (and in some cases 10-15) years, including future years, through a single process on terms that fully avoid double taxation, and the resulting benefit of avoiding transfer pricing audits in each affected jurisdiction.